By analyzing a large UK dataset, scientists have identified various financial behaviors that might point to dementia years before it leads to loss of financial capacity [1].

The money trail

Alzheimer’s disease and related dementias remain a particularly hard nut for scientists to crack. One commonly mentioned problem is that dementia is usually diagnosed relatively late, when current treatments are already ineffective. Preclinical studies have shown promising results when given at the early stages of such diseases, but in the real world, early detection in humans is a challenging task.

This creates a need for non-clinical early dementia markers, which might be hidden in behavioral patterns. However, such behaviors must leave a detectable footprint. Wearable devices are becoming more prevalent, creating a wealth of personal health data that can be used for disease diagnostics, but what if we go for something seemingly unrelated to health, like financial transactions?

Financial behavior leaves a detailed digital trail, and several recent studies have linked it to cognitive decline [2]. However, this hardly needs studies to verify, as it is well known that elderly people become less financially organized and begin falling prey to scams.

Clear signs years before loss of capacity

In a new study, published in JAMA Network Open, researchers from the University of Nottingham in the UK used banking data to investigate whether financial behaviors could serve as early indicators of a decline in financial capacity, which supposedly correlates with dementia.

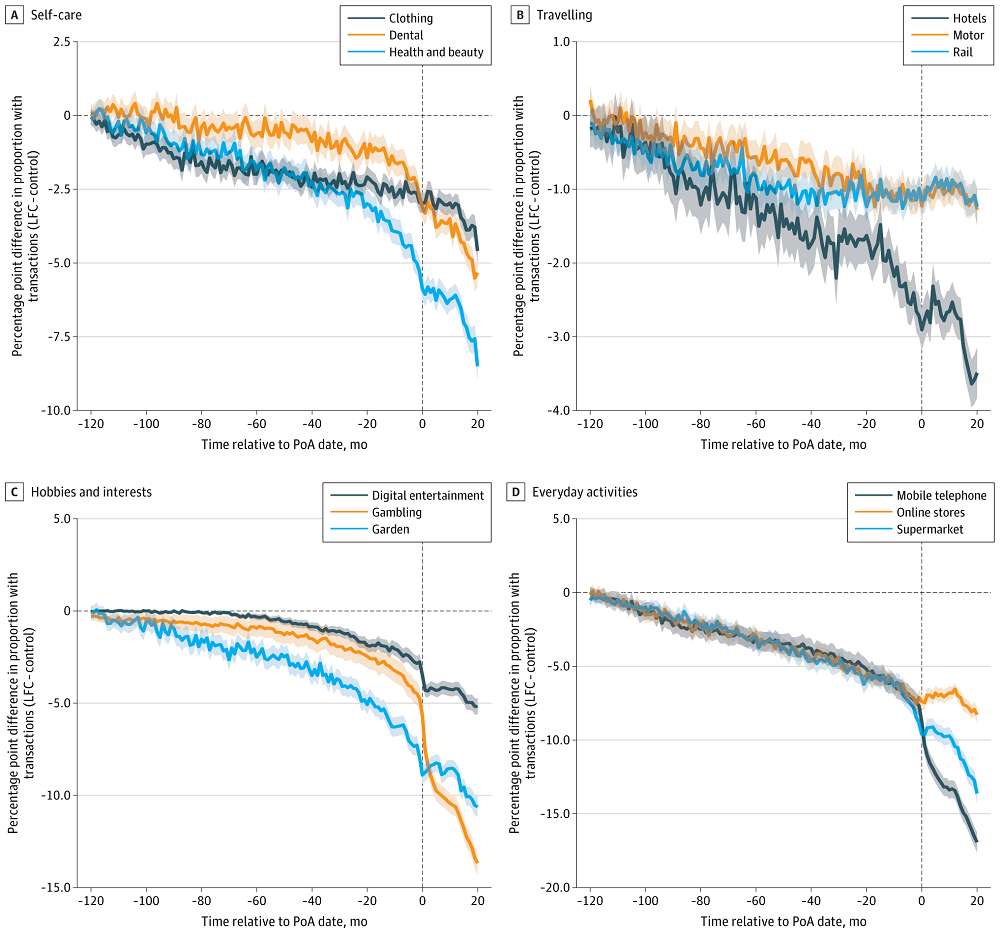

This case-control study analyzed the anonymized banking records of 16,742 people who had a “loss of financial capacity” (LFC) marker noted when a power of attorney (PoA) was registered with a major UK bank. This LFC group was compared to a control group of about 50,000 people with no reported loss of financial capacity.

The LFC group had a mean age of 72.8 years and was 61.4% female. The control group was closely matched for demographic and socioeconomic characteristics, with a mean age of 72.7 years and 61.0% being female. The study examined 344 financial measures over a 10-year period leading up to the PoA registration. To account for multiple comparisons, the researchers used a particularly robust permutation approach with 1000 iterations.

The results revealed significant differences in the financial behaviors of the two groups. Five years before the PoA registration, the LFC group, compared to the control group, showed decreased average spending on clothing by 9.1 percentage points, travel by 9.6 percentage points, and hobbies by 7.9 percentage points. Conversely, the LFC group was more likely to spend more on items associated with increased time at home, such as household gas and electricity bills, by 5.1 percentage points.

The LFC group also showed signs of heightened financial vulnerability, including more frequent PIN reset requests, an increase in reported fraud cases, more frequent reports of lost or stolen credit or debit cards, and slightly increased spending on charity. People in the LFC group demonstrated reduced attention to their finances, with a lower number of monthly online banking logins.

“These patterns provide the first large-scale evidence that behavioral data held by financial institutions can reveal the early emergence of cognitive decline,” said Professor John Gathergood, of the University of Nottingham School of Economics. “It is a powerful demonstration of how anonymized banking data can be used responsibly to protect the most vulnerable members of society.”

The data that’s already there

The study had significant limitations, the most obvious being a lack of formal diagnoses in the LFC group. While tying LFC status to dementia is a valid assumption, analyzing a sample of people with proven dementia is a more robust approach that will hopefully be explored in future studies.

Many experts think that “liberating the data” that already exists and is being gathered by various institutions can accelerate progress in biology and geroscience in particular. This, however, requires interlinked changes in regulation and public opinion. “In contrast to biomarkers,” the paper says, “cognitive and functional measures, such as behavioral financial data, are already stored in large volumes by financial institutions, which have a direct interest in protecting vulnerable customers.”

“As a society, we need to better support people at risk of losing financial capacity long before the signs become obvious to friends or family,” Professor Gathergood added. “Early detection through financial behavior may be a key part of that solution. By better understanding behavioral markers of declining capacity, banks can explore how to strengthen safeguards for customers.”

Literature

[1] Trendl, A., Anwyl-Irvine, A., Vomfell, L., Abbey, E., Stewart, N., Atkins, D., … & Leake, D. (2025). Early Behavioral Markers of Loss of Financial Capacity. JAMA Network Open, 8(6), e2515894-e2515894.

[2] Cloutier, S., Chertkow, H., Kergoat, M. J., Gélinas, I., Gauthier, S., & Belleville, S. (2021). Trajectories of decline on instrumental activities of daily living prior to dementia in persons with mild cognitive impairment. International Journal of Geriatric Psychiatry, 36(2), 314-323.